Tens of millions of Americans hold a W-2 job and earn money on the side — freelancing, consulting, selling digital products, affiliate income, coaching, or creator revenue. On paper it looks like one financial life. In practice it is two: a salary that is already taxed at the source, and business income that is taxed almost nowhere until you do it yourself.

That gap is where the avoidable mistakes live — surprise tax bills, underpayment penalties, missed retirement space, and overpaid self-employment tax. The good news is that the W-2 side, handled well, is one of the most powerful tools a side-business owner has. This blueprint shows the full structure, then walks through the five numbers that decide whether the combination costs you money or compounds it.

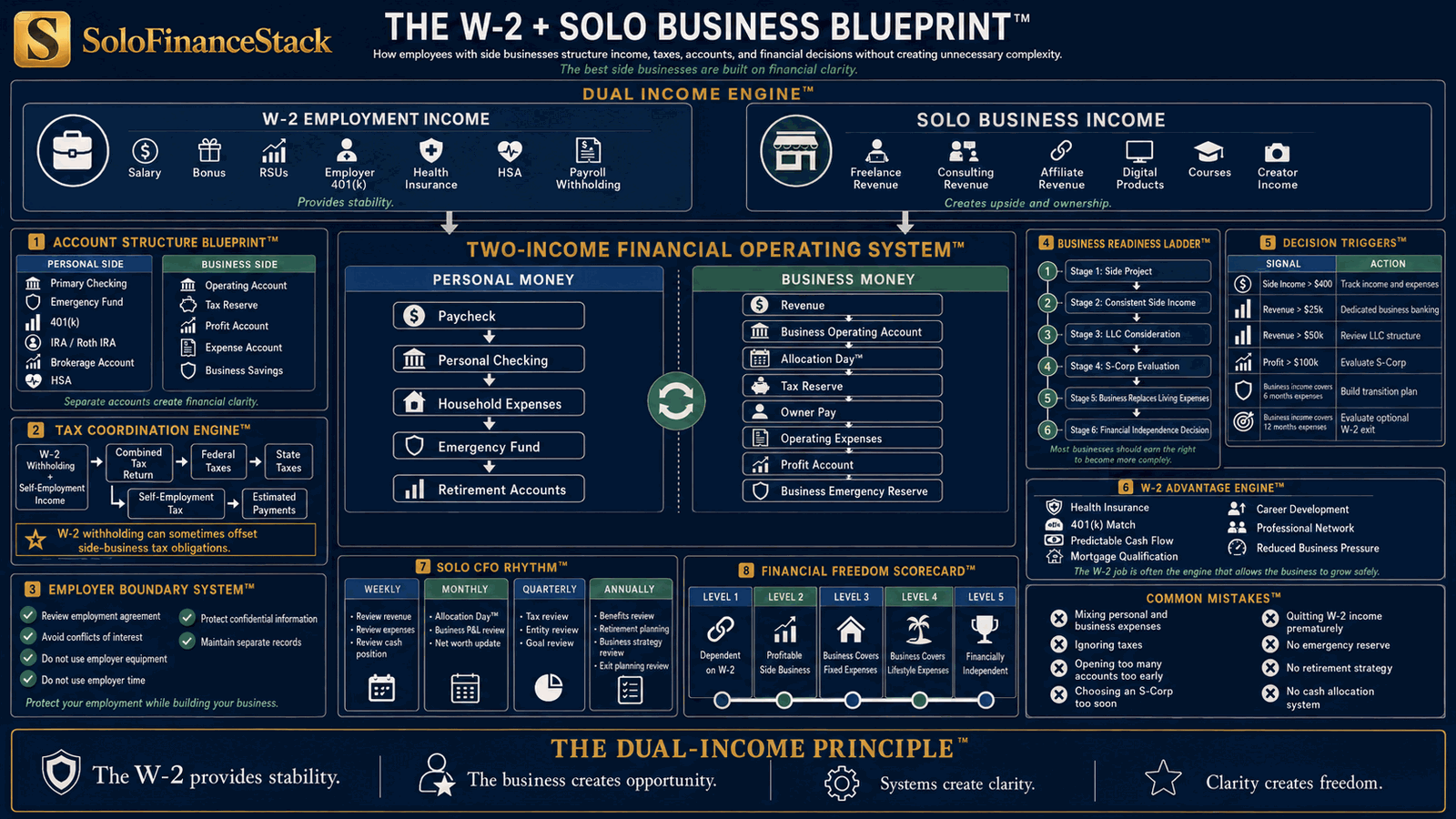

{kind=link}

Quick Answer

The rest of the blueprint is built on the same principle the diagram shows: keep W-2 money and business money in separate systems, then coordinate them deliberately at the five points where they actually touch — estimated taxes, Social Security, retirement, audit exposure, and entity timing.

1. The estimated-tax trap (and the withholding fix most people miss)

The United States runs a pay-as-you-go tax system. Your employer handles that automatically for your salary. Your side business does not — so the IRS expects you to pay tax on that income during the year, either through estimated payments or extra withholding.

You generally must make estimated payments if you expect to owe at least $1,000 after withholding and credits. You avoid the underpayment penalty if your total payments hit one of two safe harbors:

| Safe harbor | What you must pay during the year | Applies to |

|---|---|---|

| 90% rule | At least 90% of the tax shown on this year's return | Everyone |

| 100% rule | At least 100% of last year's total tax | Prior-year AGI of $150,000 or less |

| 110% rule | At least 110% of last year's total tax | Prior-year AGI above $150,000 |

Hit either applicable safe harbor and you are penalty-proof even if you still owe a large balance in April. Miss it and the IRS charges a non-deductible interest penalty on the shortfall, quarter by quarter. That rate was 8% through the first quarter of 2025 and 7% from the second quarter of 2025 through the first quarter of 2026 — it is the federal short-term rate plus three points, reset quarterly.

The practical move: estimate your side-business tax (a common starting set-aside is 25–30% of net profit for federal, more in a high-tax state), then choose your tool. Stable side income pairs well with bumped-up W-4 withholding; lumpy income pairs well with quarterly estimated payments timed to when the money actually arrives.

2. Social Security coordination: your W-2 can cut your self-employment tax

Self-employment tax is 15.3% — 12.4% for Social Security plus 2.9% for Medicare — charged on 92.35% of your net business profit, with half of it deductible against income tax. But the 12.4% Social Security portion only applies up to the annual wage base, which is $184,500 for 2026 (up from $176,100 in 2025). Medicare's 2.9% has no cap, and an extra 0.9% applies above $200,000 single / $250,000 married filing jointly.

Here is the part that helps employees with a side business: your W-2 wages count toward that Social Security wage base first. If your salary already meets or exceeds $184,500, the 12.4% Social Security portion does not apply to your side-business earnings at all — only the 2.9% Medicare portion does.

The opposite is also worth knowing: if your salary is below the wage base, your side income fills the remaining gap up to $184,500 at the full 12.4%, so the savings shrink. Either way, this is a calculation worth running before you assume your side hustle owes the full 15.3%.

You can estimate your own number with our self-employment tax calculator.

3. Retirement: the Solo 401(k) rule that trips up dual-income earners

A side business unlocks the Solo 401(k), one of the most generous accounts available to a one-person business. But there is a coordination rule that catches almost everyone who also has a 401(k) at work.

A 401(k) has two contribution types. The employee salary deferral is $24,500 for 2026 (plus an $8,000 catch-up at 50+, or $11,250 at ages 60–63). The employer profit-sharing contribution is separate, and the two together can reach $72,000 for 2026.

| Contribution type | 2026 limit | Shared with your day-job 401(k)? |

|---|---|---|

| Employee salary deferral | $24,500 ($32,500 at 50+; $35,750 at 60–63) | Yes — one limit across all 401(k) plans combined |

| Employer profit-sharing | Up to ~20% of net self-employment earnings | No — separate per business |

| Combined ceiling | $72,000 (before catch-up) | Per plan |

4. Audit reality: heightened scrutiny, not high odds

Side-business income gets a reputation for audits because it is subject to very little third-party reporting — the category where the IRS historically finds the most underreporting. That said, the headline audit rates are low for most W-2 earners.

| Taxpayer profile | Approximate audit rate |

|---|---|

| Overall individual returns | About 0.4%–0.5% (roughly 1 in 200) |

| W-2 earners, $50k–$200k income | Under 0.5% |

| $500k–$1M income | Around 1%–2% |

| Over $10M income | About 11%, projected to rise toward 16.5% by 2026 |

Most examinations are not the dramatic in-person kind — in fiscal year 2023, roughly 77% were correspondence audits handled by mail. What actually raises a side business's risk is pattern-based, not income-based:

- Repeated annual losses, which can trigger the hobby-loss question

- Income that does not match the 1099-NEC and payment-app records (Venmo, PayPal, Stripe, Etsy) the IRS already has

- Outsized home-office, vehicle, meal, or "business travel" deductions relative to your income

- Cash-heavy operations

The defenses are unglamorous and effective: report every dollar that has a matching information return, keep a separate business bank account and clean books, and document the deductions you take. Keep records for at least the standard three-year window — six years if you ever omit more than 25% of income, and indefinitely in cases of fraud.

5. Entity timing: let profit decide, not myths

"You need an LLC" and "form an S-corp to save on taxes" are the two pieces of advice most likely to be given too early. Structure should track profit, risk, and complexity. A practical evolution for a side business looks like this:

- Sole proprietor while you are testing and income is modest — fastest and simplest, no formation cost.

- LLC as revenue grows and you want liability separation and a more professional structure, especially in client-facing work.

- S-corp election only once profit is consistently high enough that payroll-tax savings clearly exceed the added payroll, bookkeeping, and compliance cost — and you can pay yourself a reasonable salary.

One more guardrail for the loss years: business losses you use to offset W-2 salary are capped by the excess-business-loss limitation, set at $256,000 single / $512,000 married filing jointly for 2026, with the excess carried forward. For a deeper walkthrough, see our guides on LLC vs. S-corp vs. sole proprietorship and the business entity guide.

The W-2 advantage most side-business owners undervalue

It is tempting to treat the job as the thing you are trying to escape. Financially, the W-2 is often the engine that lets the business grow safely. It provides health insurance, a 401(k) match, predictable cash flow, and — underrated — the income documentation that makes you mortgage- and credit-qualifiable while your business is still young and lumpy. Lenders trust two years of W-2 history long before they trust a new Schedule C.

That is the real logic of the dual-income model in the diagram above: the W-2 provides stability, the business creates opportunity, separate systems create clarity, and clarity is what eventually creates the freedom to choose whether the job stays or goes.

Frequently asked questions

Do I have to pay quarterly estimated taxes if I have a W-2 job and a side business?

Generally yes, if you expect to owe at least $1,000 on your side income after W-2 withholding and credits. You stay penalty-free by paying at least 90% of this year's tax or 100% of last year's (110% if prior-year AGI topped $150,000) through withholding and estimated payments combined.

Can I just increase my paycheck withholding instead?

Often that is the cleaner option. Because withholding is treated as paid evenly across the whole year, raising your W-4 withholding can cover side-business tax and even repair an underpayment you only catch late in the year — something a fourth-quarter estimated payment cannot fully do.

Does my W-2 job lower the self-employment tax on my side business?

It can lower the Social Security portion. The 12.4% Social Security tax applies only up to the wage base ($184,500 in 2026), and your W-2 wages count first. If your salary already reaches the base, only the 2.9% Medicare portion applies to your side income.

Can I contribute to a Solo 401(k) if I have a 401(k) at work?

Yes, but the $24,500 employee deferral is one shared limit across all 401(k)s. If you max it at work, you can still make an employer profit-sharing contribution (about 20% of net self-employment earnings) to the Solo 401(k), up to the $72,000 combined 2026 ceiling.

Will a side business get me audited?

Schedule C income draws more scrutiny, but overall odds stay under 0.5% for most W-2 earners. Risk rises with repeated losses, income that does not match 1099 and payment-app records, and aggressive deductions — not simply with having a side business.

Figures reflect tax year 2026 and were verified against IRS and SSA sources, including IRS estimated-tax and underpayment-penalty guidance (Form 2210, Topic 306, Publication 505), IRS retirement-plan contribution limits, the SSA 2026 contribution and benefit base, and IRS audit and Data Book statistics. Tax rules change and individual situations vary — this is educational content, not tax advice. Confirm specifics with a qualified tax professional.